Opportunities to serve non-traditional clients

The case for going "down market"

Over the summer I broke a window while I was edging my lawn. I’m not exactly sure how it happened, but I’m pretty sure I snagged a rock with my string trimmer and launched it into my entry way window. Every square inch of the window had a crack in it (I thought it made a pretty cool pattern).

Cold weather would be coming shortly and while I usually let projects like this fester until they become unbearable, I thought I should get someone over soon to replace it. So I scoured the internet and local friends and found a reputable company that many people trusted.

Two reps from the company came and told me they had a 3-window minimum. They said that if I were to get this window replaced I would also have to replace all my entryway windows (all of which were fine). They also made it mandatory for the estimate that they do a quick scan of the outside of the house and find any other opportunities for improvement. At the end they gave me an estimate that was much more than I was willing to pay. I let them go and said I would reach out if I wanted to move forward.

I searched the internet again, talked to some friends, and called a few companies. I found someone who came to look at the window and give me an estimate. They had no window minimums and they didn’t talk to me about other opportunities for improvement elsewhere. Instead they looked at the window for 2 mins, said they would come back the next day and replace the outside window pane in 30 min and it would cost me a fraction of what the other company would charge.

I’m sure you can see where I’m getting at here.

What I needed was someone that would replace my glass - that’s it. I was happy with the rest of my house and didn’t feel a need to fix or focus on anything else. Were there other areas of my house that could be renovated, or other windows that could be replaced? Sure, but that wasn’t important to me right then. I just needed a solution that would help our family feel safe and warm during the winter.

The opportunity for advisors to go down market

Disclaimer: most of this is driven by anecdotal evidence and not by firm data and statistics.

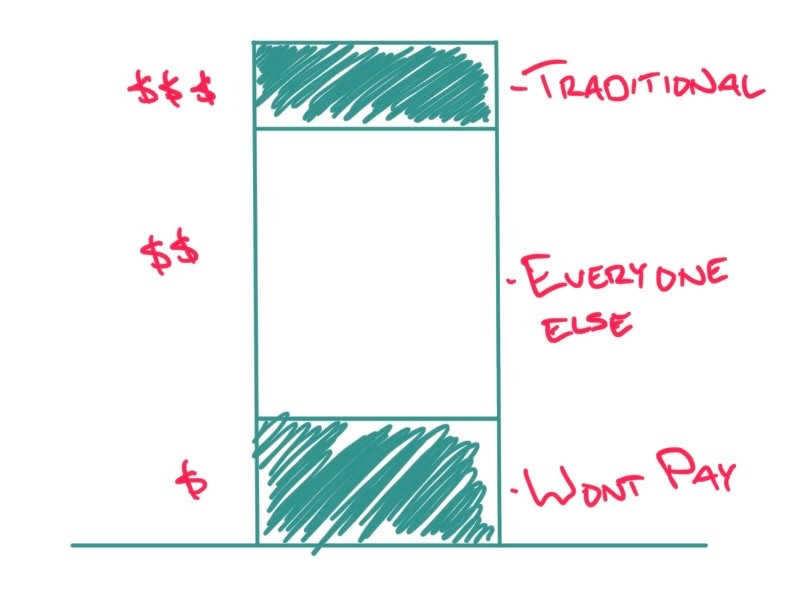

If we review the population of the US we will likely find that traditional financial advisors only really serve the top 5%-10% of the population. Anecdotally, these households are represented by having more resources to pay for financial advice (either in the form of assets to manage or through sufficient cash flow). They generally require a great deal of complex analysis and personalization.

At the bottom end of the population (in terms of net worth and cash flow) we find people that will just never pay for financial advice.

What’s interesting to me (and many others) is the middle segment representing a large chunk of the population. While these folks may not have the net worth or cash flow to pay for traditional financial advice, they are willing to pay for advice in some capacity.

Most industries or professions would look at this as an opportunity to go down market and serve more people at a lower price point. It would require a completely different service model from what other companies are engaged in. Instead of offering a high-touch, customized solution, they can offer a focused, no-fluff solution that can be repeated at scale.

How have financial advisors responded?

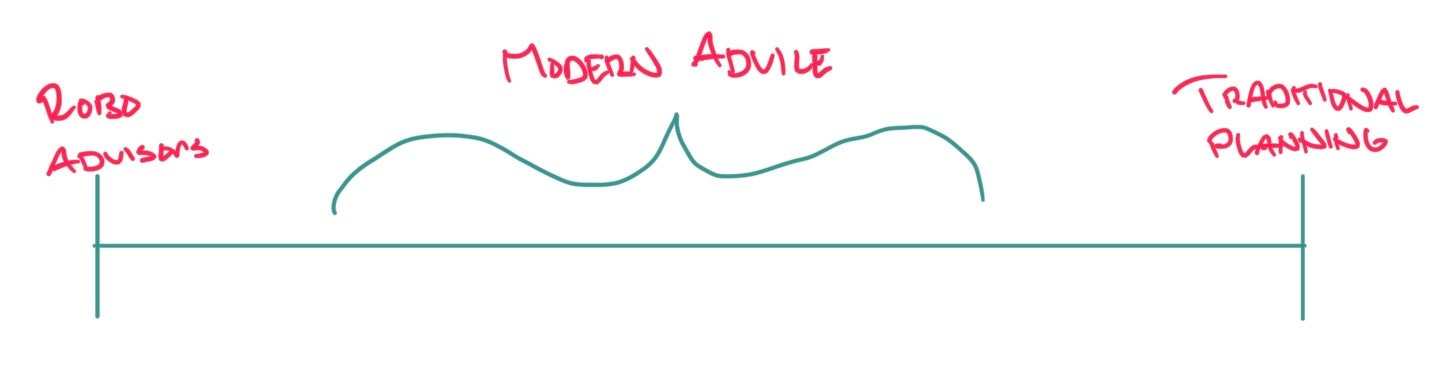

What has the financial services industry’s response been to this opportunity? Robo advisors.

We’ve seen the opportunity to go down market and essentially said “let’s let technology take over and manage the relationship for us - these folks are not profitable and therefore are not worth our time.” As you can see from the drawing below, our industry went from one end of the extreme to the other.

Robo advisors have their place, but as many of you know financial advice takes a great deal of emotional IQ and strategic communication. Both of which are very difficult for technology to take over.

How can advisors capture this opportunity?

Many financial advisors want to go down market. It may be born out of altruism, a desire to capture ideal client early in life, or purely to explore a new business strategy. Whatever the reason, we need to find where we fit on the spectrum of advice (between robo and highly customized advice).

Just like my experience with the window repair companies, there are plenty of opportunities to serve people that may not want our “full-service” offering, but who also don’t want to be handed off to AI and technology. We need to find the right balance of human engagement and technology-led interventions.

I won’t spend any more time here talking about what advisors can do and build to go downmarket. But if you subscribe to this newsletter and we’ll explore this opportunity even more.